COMPETITIVENESS FOR CANADA’S GATEWAY (2021)

Canada’s gateway sector is a key driving force for the nation’s economy, facilitating the movement of Canadian goods across the country and to international markets. Improving the climate for infrastructure investment in Canada’s gateway sector is imperative to address the growing pressures and demands on the sector, support the needs of our growing economy, ensure resilience to protect the nation from future economic shocks and to enhance our competitiveness in light of the recent U.S. tax reform.1,2 Further, enhancing the investment climate for gateway infrastructure will allow for private capacity enhancing investments that in turn support the whole national supply chain and economic recovery process.

Background

International trade is the lifeblood of the Canadian economy. Throughout Canada’s history, our open trade-based economy has successfully supported our rising standard of living. In 2018, the total value of trade in goods and services reached a record high of $1.5 trillion or 66 per cent of Canada’s GDP3.

Canada’s strong gateway sector underpins our competitiveness as a trading nation, ensuring the efficient and effective movement of vital goods through Canada and to the rest of the world. A 2018 economic impact study by the World Trade Centre Vancouver found that BC’s gateway sector alone supports nearly 310,000 jobs and contributes $34.3 billion to Canada’s GDP. 4

The onset of 2020 highlighted the national importance of railways and the gateway. Rail blockades resulted in hardships that were felt across the country as the movement of vital goods to and from communities across the country were brought to an abrupt halt. Our current reality has increased the awareness and appreciation for a robust gateway sector and the importance of maintaining the fluidity of global supply chains. The health pandemic has drawn attention to the essential service that our trade corridors and broader gateway industries provide, as they facilitated continued access to essential goods such as food and personal protective equipment (PPE) throughout the pandemic.

Over the years, the Federal Government has meaningfully invested in critical capacity enhancing gateway infrastructure projects in a way that has incented the participation of private sector partners. Investment to date have resulted in increased capacity, fluidity and efficiency of the gateway. Through the $2.4 billion National Trade Corridors Fund (NTCF), a key element of Transportation 2030, the Government of Canada has focused investments in strategic infrastructure projects to address transportation bottlenecks, vulnerabilities and congestion along Canada’s trade corridors.5 As of February 2020, more than $1.7 billion had been committed to through the NTCF for 82 marine, air, rail and road projects.6 These important initiatives help Canadian companies access and compete in key global markets and trade more efficiently with international partners.

However, the importance and relevance of trade is only expected to grow for Canada; the federal government’s 2018 Fall Economic Statement set the target of increasing Canada’s overseas exports by 50 per cent by 20257. Implementing mechanisms that encourage investments in Canada’s gateway sector will help expand the capacity and efficiency of our trade enabling infrastructure, which will be critical as our country prepares for economic recovery and beyond to prosperity.

The role of rail

The gateway sector is composed of the mix of industries whose main business activity is to facilitate trade activity. The railway industry is a key enabler for this sector as it connects our nation with our terminals and ports and the rest of the world.

Rail operators are an integral segment to Canada’s gateway sector, as it transports approximately $328 billion of Canadian-originated goods each year, with freight rail moving 50 per cent of exported goods.8 Each year, approximately 3,800 locomotives and 32,800 dedicated railroaders transport goods and people across 44,000 kilometers of rail track across Canada and several points in the United States. 9 These tracks require maintenance and upkeep to ensure efficient deliveries, but more importantly to ensure the safety of rail employees and the communities in which they operate.

The railway industry is uniquely positioned to reduce greenhouse gas (GHG) emissions while supporting the economy and enabling trade. Railways are among the lowest industrial emitters in Canada, accounting for just 1% of GHG emissions. Despite increasing demand, railways continue to achieve emissions reductions. Since 1990, freight railways have reduced their GHG intensity by more than 40%, while experiencing an 80% increase in workload, 10

Rail plays an increasingly vital role in Canada’s trade corridors, particularly as it pertains to moving Canadian agricultural products. Canada's two largest railways, CN and CP, moved a record 15.4 million tonnes of grain in the final three months of 2019: CP set a new quarterly record by moving 7.9 million tonnes of grain and grain products and CN transported 7.5 million tonnes, which included an all-time monthly record of 2.79 million tonnes in October 2019 and the second best December on record despite a work stoppage.11

Rail is one of Canada’s most capital-intensive industries and grain is one example of how important railway companies’ annual spend on continuous improvement and maintenance is to the economy. Canadian railways are vertically integrated and own the track, real estate, and locomotives and rolling stock, which illustrates the need for significant investments. On average, Canadian railways invest between 20 and 25 per cent of their own revenues back into their networks each year — close to $30 billion in Canada alone since 1999.12 These significant annual investments into rail infrastructure, support the strong and growing demand for Canadian products and supports the fluidity of getting Canadian products to global markets.

The need for a more competitive playing field

Canada needs a competitive tax framework to further incent railway infrastructure investment to ensure that the sector continues to have the ability to facilitate future volume growth including future demands for a growing gateway.

The recent U.S. Tax Reform has allowed for an even faster tax write-off of investment dollars compared to Canada. This has resulted in the after-tax-cost of investing in infrastructure to be higher in Canada than the U.S. New U.S. tax measures increased the bonus depreciation available in the year of acquisition from 50 per cent to 100 per cent for most property/capital acquired after September 27, 2017 and before

January 1, 2023. While the Canadian Government tried to address this issue broadly in its 2018 Fall Economic Statement, their efforts not only fell short of the US Tax Reform but did not even come close to the US pre-reform rate of 50 per cent write-off in the first year.

With a lower after-tax-cost in the U.S., Canadian railways and customers, who invest in their own rail infrastructure, are at a tax disadvantage to U.S. railways. If this tax imbalance persist important economic opportunities and investments in Canada may be being forgone.

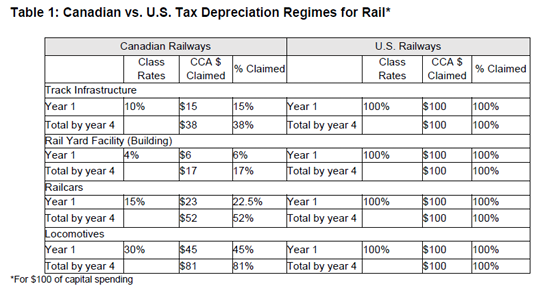

The following table highlights the differences between the Canadian and U.S. tax regimes as they relate to railway capital spending.

As recent U.S. tax reforms have altered the competitive landscape in North America, tax changes in Canada must ensure that the rail section and investment in rail infrastructure remains competitive. An important manner in which this can be achieved is through accelerated depreciation on capital investment. This significant measure would ensure that railways continue to make investments that improve safety, environmental performance, and enhance capacity to meet the needs of customers and the Canadian economy.

THE CHAMBER RECOMMENDS

That the Federal Government:

- Enhance the depreciation regime for rail infrastructure investment to promote greater investment in rail infrastructure, to support BC’s competitiveness as a trade Province, and to meet the needs of the growing national economy and trade volumes; and

- Continue working with gateway industries and stakeholders to explore a policy framework, including tax measures, to incent investment in necessary capacity enhancing gateway infrastructure.

1 In the United States, in 2017, the Tax Cuts and Jobs Act reduced the federal statutory corporate tax rate for U.S. companies from 35% to 21%, while the Base Erosion and Anti-Abuse Tax (BEAT) minimum tax increased costs for Canadian railways. This provision forces U.S. entities to pay the BEAT on payments made to foreign affiliates, without a corresponding offsetting credit or deduction for the equivalent amount of BEAT paid in the U.S.

2https://www.congress.gov/bill/115th-congress/house-bill/1/text

3https://www.international.gc.ca/gac-amc/assets/pdfs/publications/State-of-Trade-2019_eng.pdf

4https://www.boardoftrade.com/wtcref/

5https://www.tc.gc.ca/en/programs-policies/programs/national-trade-corridor-fund-backgrounder.html

6https://www.tc.gc.ca/en/programs-policies/programs/projects.html

7https://www.budget.gc.ca/fes-eea/2018/docs/statement-enonce/chap03-en.html

8 CANSIM Tables 23-10-0062-01, 23-10-0063-01, 23-10-0216-01, Rail Trends Database, CN, and CP

9 2018, Rail Trends Database

10https://www.railcan.ca/wp-content/uploads/2019/08/August_2_-2020_Prebudget_Submission-_RAC_FINAL.pdf

11https://www.cbc.ca/news/canada/calgary/grain-cp-cn-train-rail-shipping-fourth-quarter-1.5417334#:~:text=Canada's%20two%20largest%20railways%20moved%20a%20record%2015.4%20million%20tonnes,of%20gr ain%20and%20grain%20products.