ADDRESSING BARRIERS TO SUCCESSION PLANNING FOR SMALL TO MEDIUM ENTERPRISES (2022)

Innovation, Science and Economic Development Canada defines an SME when a business employs anywhere from 1 to 499 employees, which includes Micro-enterprises employing 1 to 4 individuals.

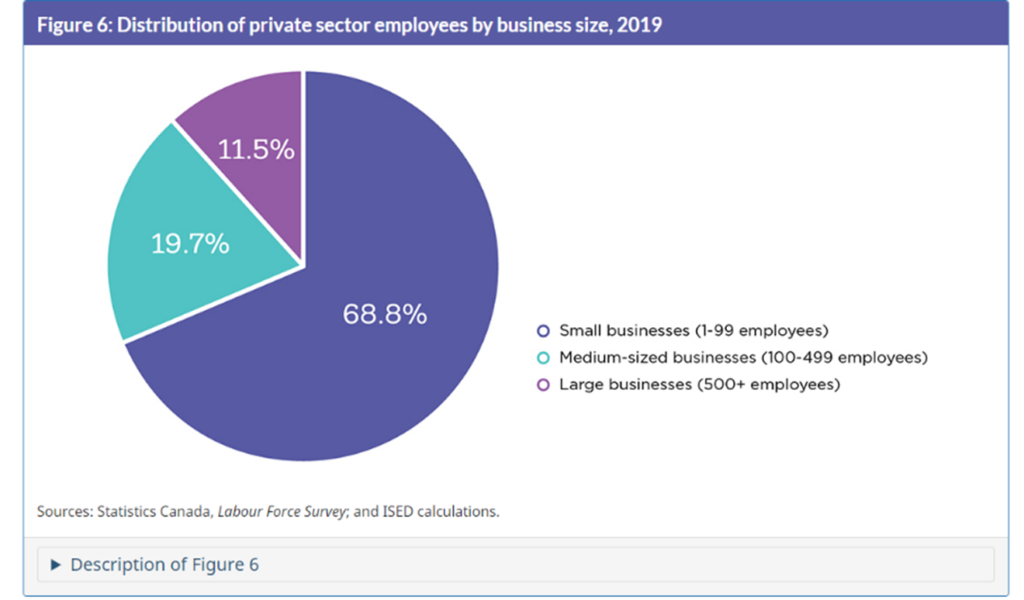

In Canada, as of 2019, small businesses employed 8.4 million individuals, or 68.8 percent of the total private labour force. By comparison, medium-sized businesses employed 2.4 million individuals (19.7 percent of the private labour force) and large businesses employed 1.4 million individuals (11.5 percent of the private labour force). Between 2014 and 2019, small businesses were responsible for 35.8 percent of the net employment growth in the private sector, which increased by approximately 772,200 jobs. Medium-sized businesses contributed 25.4 percent of this net employment growth and large businesses contributed 38.8 percent [1].

The importance of small and medium sized enterprises to the national economy and the need for succession planning and the creation of a business exit strategy should not be underestimated.

Background

From 2021 to 2031, the BC Labour Market Outlook analysts project over 1 million job openings in British Columbia [3]. In addition to the pressures of transitioning our businesses to the next generation, the population and the labour force will continue to age, and employers will need to replace retiring workers at an increasing rate.

Anticipating the generational shift, succession planning is key—but only 34% of Canadian family businesses have a robust, documented and communicated succession plan in place. SME businesses need professional support and moderation to address them properly [4].

To ensure business owners successfully accomplish the transition of their business, it is essential to have the necessary tools and resources at their disposal.

A succession plan helps a business owner deal with complex topics such as:

- tax issues;

- required qualifications and skills of successors;

- legal issues;

- how the successor will be trained/prepared for the role; and

- mechanics for the purchase or transfer.

Some of the top barriers to succession planning include but are not limited to:

- finding a suitable successor;

- valuing a business;

- financing for the successor; and

- access to cost effective professional advice.

British Columbia’s Venture Connect program offeredthrough Community Futures prepares businesses for a sale so they can be transferred to a new owner – keeping businesses in our communities. Venture Connect began as a project created in response to the challenge that over the next 20 years, there will be unparalleled shortfalls of both business owners and employees resulting in potential closure of large numbers of small businesses throughout the province. Even with resources such as Venture Connect, SMEs have historically been, and continue to be, vulnerable with respect to receiving approval for financing from lending institutions. This not only includes entrepreneurs starting a brand-new business, but also those looking to purchase an existing business, as in the case of succession.

Under the direct investment model, a small business in BC can register as an eligible business corporation (EBC). EBCs can accept equity capital directly from investors without having to set up a venture capital corporation (VCC). This investment structure is intended to assist investors planning to be actively involved in the growth of a small business [5]. However, the current program is not inclusive towards small and medium size businesses involved in a succession transaction.

Continued government funding towards existing, revised and new programs that support business owners transitioning their businesses, is imperative to maintaining a healthy economy.

On June 29, 2021, the Senate approved Bill C-208, which attempts to correct “unfair” income tax impacts that can arise when shares of private businesses are transferred to family members.

Prior to Bill C-208, individuals were generally financially incentivized to sell the shares of their business to an arm’s length party rather than to the next generation [6].

Bill C-208 facilitates intergenerational transfers by excluding the application of the punitive deemed dividend rules on transfers of a qualified small business, family farm or fishing corporation to a related party, provided that the purchasing corporation is controlled by one or more children or grandchildren over the age of 18, and the purchasing corporation does not dispose of the acquired corporation within 60 months of the transfer [7].

On July 19, 2021 the Federal Department of Finance announced that it proposes to introduce additional amendments to Bill C-208 due to concerns that it may inappropriately facilitate tax-motivated business transfers within families, where there is no intention of having the business carried on by the next generation such as:

- the requirement to transfer legal and factual control of the corporation from the parent to the children or grandchildren;

- the level of ownership in the corporation that the parent can maintain after the transfer; and

- the requirements and timeline of the transition of the business of the corporation from the parent to the children and grandchildren, and the level of involvement of such children or grandchildren in the business after the transfer.

While these are significant advances in reducing the burden on businesses looking to transfer their business to the next generation, more needs to be done to support business owners with the appropriate tools and legislative reform to keep the doors of our businesses open.

Since 2013, several tax measures have been introduced to assist Canadian business owners with the transition of their businesses. The Lifetime Capital Gains Exemption (LCGE) is one very important tax measure because for many business owners, the sale of their business is their retirement income.

The Lifetime Capital Gains Exemption (LCGE) is a federal tax deduction that can be claimed against taxable capital gains on the disposal by an individual of:

- qualified small business corporation (SBC) shares;

- qualified farm property; and

- for dispositions for qualified fishing property.

The LCGE is indexed to inflation. LCGE for qualified farm or fishing property dispositions is the greater of:

- $1 Million; and

- the indexed Lifetime Capital Gains Exemption applicable to capital gains realized on the

- disposition of qualified small business corporation shares.

Amending the LCGE to include all SMEs attempting to legitimately and lawfully transition their businesses to the next generation will help to counterbalance the forecasted labour shortages, increasing retirement levels and assist with keep our businesses open and our communities strong during these challenging times.

It would be prudent for government to focus on stimulus for succession planning for small business that addresses the various business structures while keeping in mind that vendor’s general desire to use the Federal Tax Act provisions to minimize tax on the transition.

Overall, there is a continued need for awareness to the issue of succession planning for SMEs as well as additional changes to existing government resources, programs and legislation to provide sellers and potential purchasers the incentives to conduct succession planning and transition their businesses effectively.

THE CHAMBER RECOMMENDS

That the Provincial Government:and, where applicable, the Federal Government:

- Review the current “qualifying activities” in the existing Eligible Business Corporation (EBC) program and:

- Include a clause which allows the program to be more inclusive towards small to medium sized businesses in a succession transaction;

- Include a vendor financed arrangement as a qualifying activity, whereby the vendor will receive the same 30% tax credit for financing the business succession transaction, thereby reducing the vendor’s risk.

- Expand the scope of existing small business financing programs to incorporate succession planning as a legitimate reason for small business financing.

- Allow small corporations to defer the tax on the capital gains from the transfer of a business to the owner’s children.

- Increase the Lifetime Capital Gains Exemption amount to $1 million for all SMEs.

- Ensure that future amendments to the Income Tax Act do not impede legitimate and lawful intergenerational transfers of small businesses to family members and are considered with terms that are, at minimum, equitable with those when transferred to any third party.

[1] Key Small Business Statistics, Innovation Science and Economic Development Canada 2020 Report, page 17

[2] Key Small Business Statistics, Innovation Science and Economic Development Canada 2020 Report, page 17

[3] BC Labour Market Outlook 2021-2031 Forecast 2021 Edition, page 5

[4] https://www.pwc.com/ca/en/private-company/family-business-survey-canadian-insights-2021.html

[5] https://www2.gov.bc.ca/gov/content/employment-business/investment-capital/venture-capital-programs/eligible-business-corporation

[6] https://www.richardsonwealth.com/news/intergenerational-business-transfers

[7] https://www.richardsonwealth.com/news/intergenerational-business-transfers